‘Gates have opened’ for in-plan annuities, LIMRA Research Director says

Legislative changes, product development and an enthusiastic industry are opening the gates to annuity products inside retirement plans.

Still, analysts are cautiously optimistic about the next steps. Challenges remain, said Alison Salka, senior vice president, director of research, for LIMRA and LOMA.

"The gates have opened, and you now have guidelines for portability, which was a question," Salka said. "So the gates have opened, but they haven't been floodgates, because I think the market is still nascent."

Salka will participate today in a session titled, "In-Plan Annuities: Are We at the Tipping Point for Adoption?" at the LIMRA 2023 Annual Conference at National Harbor outside Washington, D.C.

Momentum is definitely high, Salka said, fueled by the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 and the follow-up SECURE Act 2.0, signed into law in December. The bills removed barriers to offering annuities inside retirement plans, and the industry has responded.

"We're starting to see now are a lot of innovations and new products, especially since SECURE," Salka said. "We've been tracking sales and so far it's been a relatively staid market. But we are at a point where you're seeing more interest. You are seeing things change."

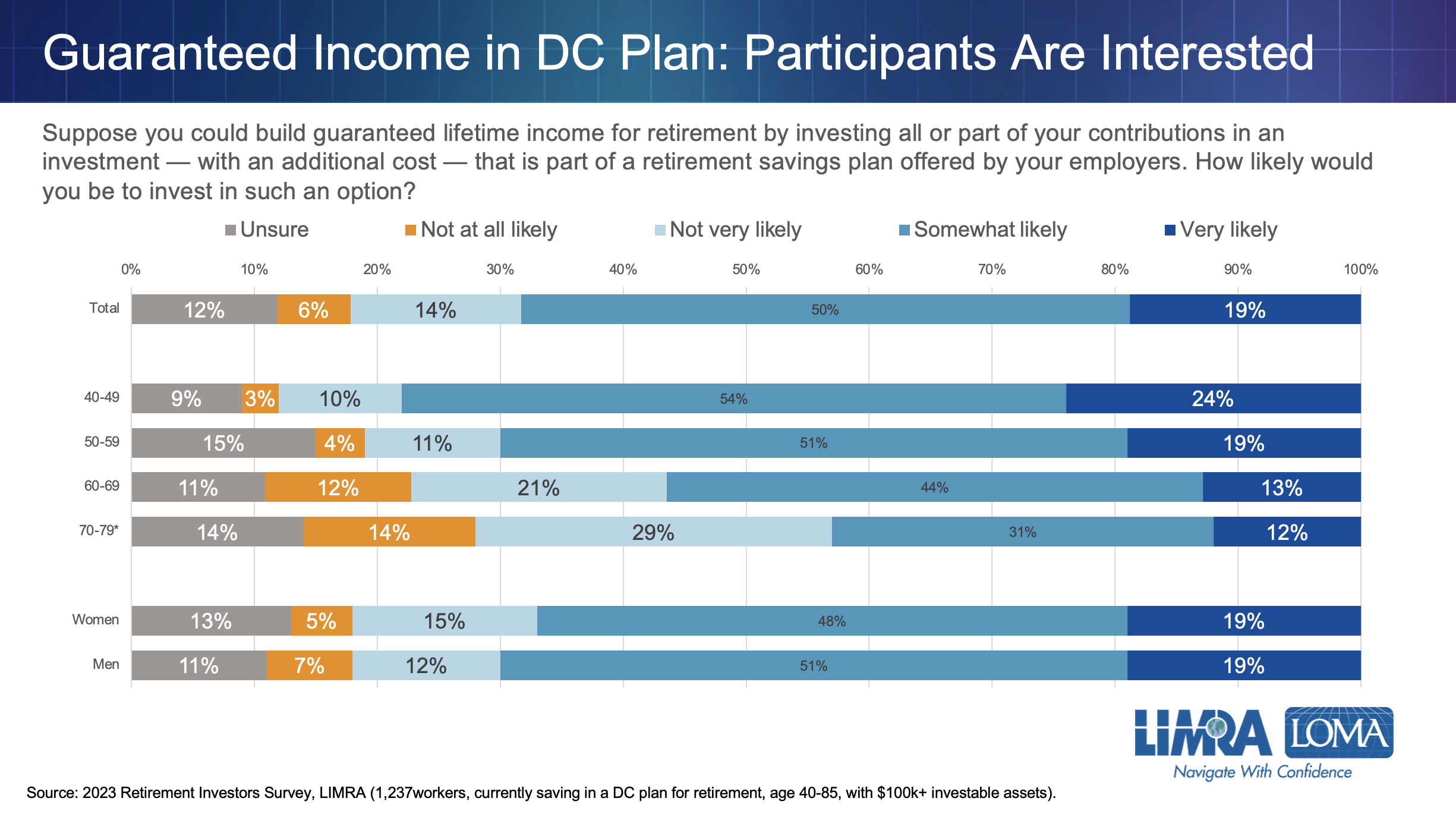

Americans want income

Supply naturally follows demand and in-plan annuities must have a market to thrive. The 2023 LIMRA Retirement Investors Survey of consumers shows a gathering market for guaranteed income.

"I think participants have always recognized that benefit," Salka said. "That is one hurdle, educating them about it, helping them take the steps, getting them into a plan that has [guaranteed income] available. Certainly we know that participants are interested and we know that defined contribution plans, retirement plans are where most of retirement assets are."

Complexity and availability remain the two biggest hurdles to in-plan annuities, a separate LIMRA/LOMA advisor survey revealed. Thirty percent of advisors said the products are "difficult for a sponsor to understand," while another 28% said "products are not available on all recordkeeping platforms."

Not surprisingly, better-educated advisors is a big key to connecting lifetime income products with eager plan participants.

"It seems like efforts to educate advisors and consultants has been working," Salka said. "So it seems like advisors and consultants are in a better position today to advise on these products and they're more comfortable recommending them."

Target-date products

One annuity in-plan product design that is gaining favor is the target-date fund with an annuity component. One popular design calls for gradual purchases of deferred life annuities beginning at age 50, instead of increasing the allocation to bond funds.

The National Bureau of Economic Research published a paper earlier this year finding that allocating a portion of target-date assets to deferred life annuities is financially beneficial compared with leaving all assets in a target-date fund and purchasing an immediate annuity at retirement.

"The target-date design has been one that we have found that advisors are more familiar with and makes sense, but I don't think it's the only option," Salka said. "What you're seeing right now is innovation and experimentation to see the different ways to meet this need. And I think that's a good thing."

InsuranceNewsNet Senior Editor John Hilton covered business and other beats in more than 20 years of daily journalism. John may be reached at [email protected]. Follow him on Twitter @INNJohnH.

© Entire contents copyright 2023 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Advisor News

- The overlooked retirement security risk that must be addressed

- What advisors should know about hedge funds in retirement planning

- Retirement control is top success measure for middle class, ACLI says

- Industry groups applaud House passage of Financial Exploitation Prevention Act

- Younger workers more likely to be eligible for a retirement plan after changing jobs

More Advisor NewsAnnuity News

- Malibu Life Holdings Completes Acquisition of TruSpire, Establishing Malibu USA and Accelerating Entry into the U.S. Retail Annuity Market

- Why job boards are failing insurance agencies

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

- What’s fueling record annuity growth?

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

More Annuity NewsHealth/Employee Benefits News

- Researchers from City University of New York (CUNY) Detail New Studies and Findings in the Area of Mental Health Diseases and Conditions (The effect of Medicaid reimbursement for psychiatrists on the health care burden of serious mental illness): Mental Health Diseases and Conditions

- Recent Reports from Chungbuk National University Hospital Highlight Findings in Stomach Cancer (A 5-year mortality-prediction model for patients with stomach cancer, based on the Korean nationwide health insurance claim database): Oncology – Stomach Cancer

- NH Dems decry Medicaid premium increases

- If we lose our coverage, we lose our lives | PODIUM

- Rural Texas Is Losing Affordable Care Access Coverage Even as Statewide Enrollment Rises

More Health/Employee Benefits NewsLife Insurance News

- NAIFA praises House committee approval of Clarity for Compensation Act

- PHL Variable liquidation pushed out to 2027, Connecticut regulators say

- ‘Recession-Proof’ Insurance Is Trending. Safety Net or Scam?

- Winged Keel Group Expands National Presence and PPLI Leadership, Welcomes SBSI, Inc. (dba NFP Insurance Solutions)

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

More Life Insurance News