A More Balanced Approach to Comparing Policy Illustrations

Factoring in non-guaranteed elements adds objectivity

Life insurance illustrations are designed to provide clients some perspective on how their policy may perform over time, based on unchanging assumptions. However, assumptions are inherently variable. Let’s take a look at indexed universal life insurance policies and some of the factors involved, including how you might level the playing field.

THE ART OF THE ILLUSTRATION

Since interest crediting is a selling point and a concept most clients understand, it’s commonly used as a way to compare carriers and as a differentiator on illustrations. We run illustrations using assumptions based on the current environment. However, assessments of the environment and appropriate assumptions are open to interpretation.

In reality, no one knows what the future holds. Crediting rates are not guaranteed and will vary unpredictably over the long term. But interest crediting is not the only non-guaranteed element of a policy. Policy fees and charges can also vary. In fact, several carriers have recently taken to raising non-guaranteed charges on in-force blocks. You just don’t know how long current charges will apply or how often they will change. What we do know are the charges today and maximum charges allowed by the policy.

As a result of these factors, illustrations are required to contain various scenarios to help paint the picture. Every illustration shows policy performance based on:

- Interest rate assumptions and current charges

- An alternate scenario of level fixed account crediting with current charges

- Mid-point values between current and guaranteed charges and credits

- Guaranteed minimum crediting and maximum charges

Clients need you — their agent — to help interpret it all and compare their options. With interest crediting volatility and charges that are not locked in, how can you be sure you are comparing apples to apples?

A MORE BALANCED APPROACH

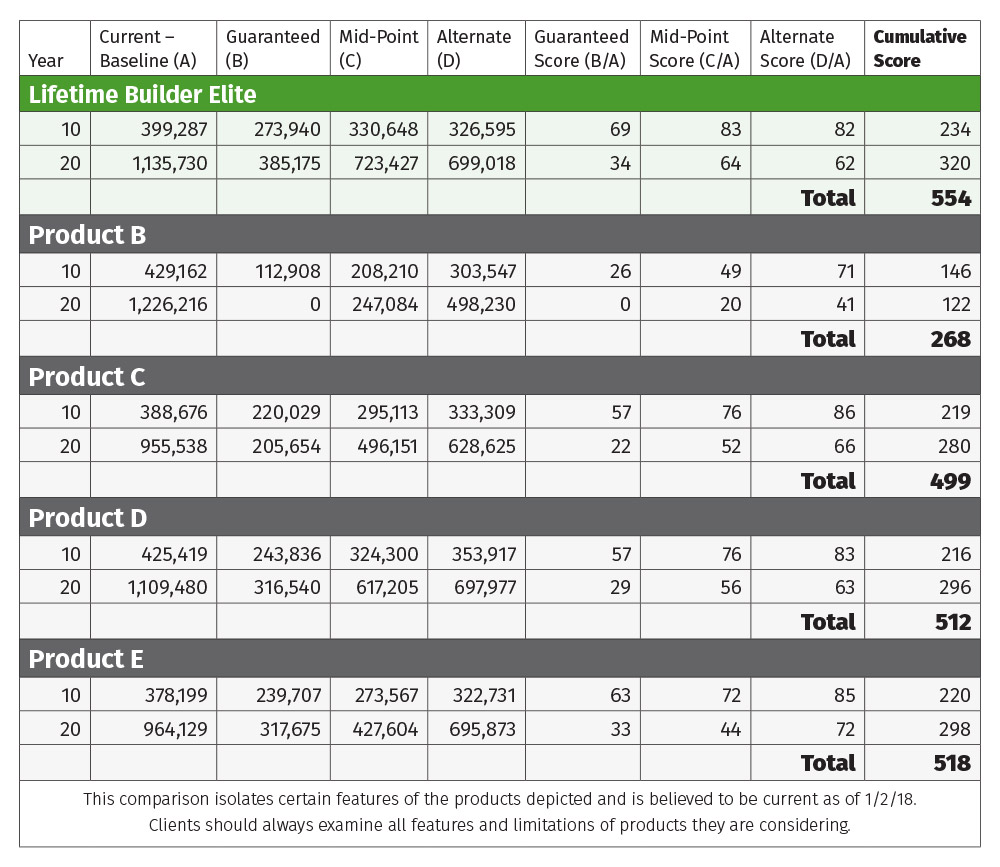

Comparing cash surrender values over time to current account values could be a tool to help level the playing field and provide a more objective comparison of products, given the nature of non-guaranteed elements. To devise a scale and formula:

- Assume a cash surrender value that equals the current ledger’s account value earns a score of 100.

- If the surrender value is half that of the account value, it earns a score of 50, and so on.

- Using a weighted average at both 10- and 20-year durations, available in illustrations, add scores for guaranteed, alternate and mid-point scenarios.

- Combine the cumulative results of the two durations for a total score for comparison.

Take a look at the accompanying table to see how it looks using different products on the market today, starting with Global Atlantic’s Lifetime Builder Elite. The higher the score, the less susceptible cash surrender values will be to changes in non-guaranteed assumptions.

Next time you’re presenting an IUL product to a client, try this little experiment for a more balanced approach to comparing policies. For more information please visit www.GlobalAtlanticLife.com.

Next time you’re presenting an IUL product to a client, try this little experiment for a more balanced approach to comparing policies. For more information please visit www.GlobalAtlanticLife.com.

Tom Doruska, FSA, MAAA, is Senior Vice President, Life Products, at Global Atlantic, and Chair of the ACLI IUL task force.

The Future of Underwriting in the Palm of Your Hand

5 important steps a client should take following an auto accident

Advisor News

- How smart investments prepare clients for inflation

- Amid slew of corporate tax ideas, Newsom chose one likely to hit people’s premiums

- The biggest risk to your clients’ financial plans isn’t market volatility

- Initiative looks at how caregiving impacts workplace benefits

- Will rising retirement needs spark an annuity boom?

More Advisor NewsAnnuity News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- Fortitude Re Completes $500 Million FABN Issuance

- Reframing retirement income for greater certainty

- Jackson Introduces Dow Jones Industrial Average Index Option, Flexible Premiums, Six-Year Rate Guarantee in Latest Registered Index-Linked Annuity Launch

- Senior Market Sales® Fortifies Annuity Reach With Acquisition of Retirement Planning Firm Stratton & Company

More Annuity NewsHealth/Employee Benefits News

- Final rules for Medicaid work requirements are out. Here's what you need to know.

- Final rules for Medicaid work requirements are out. Here's what you need to know.

- Hyde-Smith blasts health care delays

- WNY health insurers seek rate hikes of 9% to 24% for 2027

- Healthcare now costs more than mortgages

More Health/Employee Benefits NewsLife Insurance News

- AM Best Affirms Issue Credit Ratings of Weston2038 LLC’s Credit-Linked Notes

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- Greg Lindberg moves to halt $1.65B restitution order, claims he ‘overpaid’

- Fidelity Investments® to Expand Target Date Lineup With Launch of Guaranteed Income Solution

- KBRA Releases Research – Private Credit: Much Ado About Nothing – Perspectives on Columbia Business School Paper About Private Ratings

More Life Insurance News