Smoking Can Send Life Insurance Premiums Ablaze

By Mike Brown

Lend EDU

Although naturally grim in its circumstance, life insurance can be an important safety net for a policyholder’s loved ones.

But having life insurance comes at a cost, so consumers must weigh the pros of paying for a policy against the potential consequences of not having one.

That cost depends on the policy and the person. Things like age, medical history, current health, and smoking habits can alter a person’s annual life insurance premium.

For example, because smoking is detrimental to a person’s health, policies for smokers are more expensive to account for the increased likelihood of mortality within the policy term.

Just how much can smoking increase a life insurance policyholder’s premium?

To answer this, LendEDU teamed with BestLifeRates, an independent life insurance marketplace. Using exclusive data from about 35,000 life insurance policy quotes provided by BestLifeRates, LendEDU analyzed the dollar difference in life insurance policy quotes between smokers and non-smokers.

How Smoking Affects Life Insurance Costs

The data featured in this report was anonymized and provided exclusively to LendEDU from BestLifeRates. Users can go to BestLifeRates.org, enter their personal information, and receive life insurance quotes based on their circumstances, including whether they are a smoker.

BestLifeRates works with NinjaQuoter to gather the data and provide quotes to users.

On Average, Smokers Will Pay Nearly Double the Life Insurance Premiums of Non-Smokers

As the above graphic illustrates, the data shows smokers, on average, will pay nearly double for life insurance premiums what non-smokers will pay.

The average annual life insurance premium BestLifeRates quoted for smokers was $3,977, while this figure was $2,052 for non-smokers. These figures indicate that smoking could increase life insurance premium costs by 94%.

The average annual life insurance premium quote for the entire dataset, including both smokers and non-smokers, was $2,241.

The above figures do not account for things like age, type of policy, or coverage amount. We’ll look at those below.

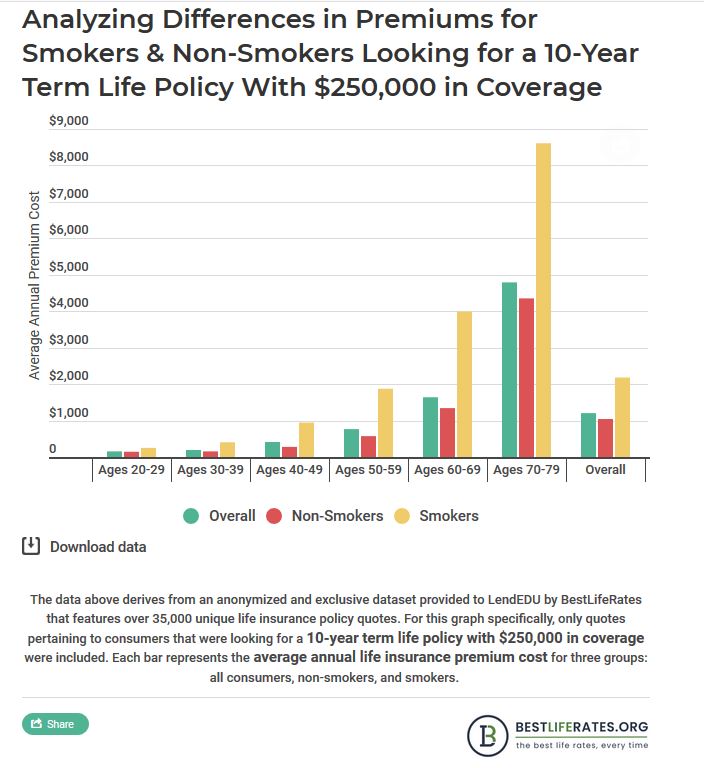

The graphic above represents all consumers who requested a quote for a 10-year term life insurance policy with $250,000 in coverage. This breakdown shows how smoking can impact annual life insurance premium quotes for consumers who were all looking for the same life insurance product.

With nearly every age group, with the exception of the youngest and oldest, smokers got life insurance quotes with annual premiums that were more than double those non-smokers received.

When age was not factored in, smokers in this subsection collectively got quotes for their premiums that were 109% more than what non-smokers got.

Removing smoking from the equation, the graph also depicts how age greatly impacts what people may pay for life insurance policies. For example, while the average annual premium quoted for those in their 20s was $155, it was $4,793 for those in their 70s.

This is because, as a consumer gets older, their health risks generally increase, making them riskier for life insurance companies.

Methodology

All data found in this report was anonymized and provided exclusively to LendEDU by BestLifeRates, an independent life insurance marketplace. The dataset features over 35,000 unique life insurance quotes that were provided to visitors of BestLifeRates.org who were looking for a life insurance policy quote based on their unique circumstances.

BestLifeRates works with NinjaQuoter to collect and analyze the user data to provide life insurance policy quotes.

The data that was included in this report has been collected over an extended period of time, starting in October of 2016 and ending in September of 2019. The data includes things pertinent to providing a life insurance policy quote, like smoking habits, age, location, coverage amount sought, and whether the consumer was looking for a whole life or term life policy.

The annual premium amounts that were quoted for each consumer are projections made by BestLifeRates and NinjaQuoter and may not accurately reflect the terms that the consumer ended up receiving. Additionally, specific types of smoking habits that may alter the life insurance policy rate were not specified, including whether the consumer was vaping, smoking cigars or cigarettes, or smoking marijuana.

Illinois’ congressional delegation backs Pritzker’s appeal to FEMA after help denied to flood survivors

Workers Gamble With Health Insurance Benefits, Unum Finds

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Douglas Veterans Claims Clinic Connects Rural Veterans With Critical Services

- Atrium pushes back after State Health Plan leaves healthcare network out of Tier 1

- Connecticut health insurance exchange shifts enrollment dates after federal changes

- Iowa health insurers propose premium increases for ACA customers

- NEW REPORT: THOUSANDS OF IOWANS FACING HIGHER HEALTH INSURANCE PREMIUMS NEXT YEAR THANKS TO ASHLEY HINSON

More Health/Employee Benefits NewsProperty and Casualty News

- COLUMN: Military members, families: Check out these insurance tips

- Homeowners of color pay higher insurance costs in WA, nationwide

- Loews Corp. (NYSE: L) Highlighted for Surprising Price Action

- Charleston ranks 10th-riskiest US county to insure. Here’s how much it costs

- Travelers Reports Excellent Second Quarter and Year-to-Date Results

More Property and Casualty News