Spenders Into Savers: The Great American Shift

Although Americans may be known globally as ravenous consumers, they are more likely to call themselves savers, a title they earned over the pandemic, according to some reports.

The Federal Reserve confirmed in its latest report that Americans are saving buckets of cash since the start of the pandemic, often related to federal stimulus infusions.

From the end of the Great Recession to February 2020, the personal saving rate averaged 7.25% until the beginning of the pandemic. The rate shot up to 17.9% since then.

The 2020 savings spike was so significant, it dwarfed the previous half-century’s rates.

The Fed noted that families might be saving as a precaution in uncertain times, but much of the saving has to do with the inability to spend during the lockdowns. In fact, the rate has been dropping since March when the savings rate spiked to 26.9% and has since dropped to 9.4%, which still exceeds the average before the pandemic.

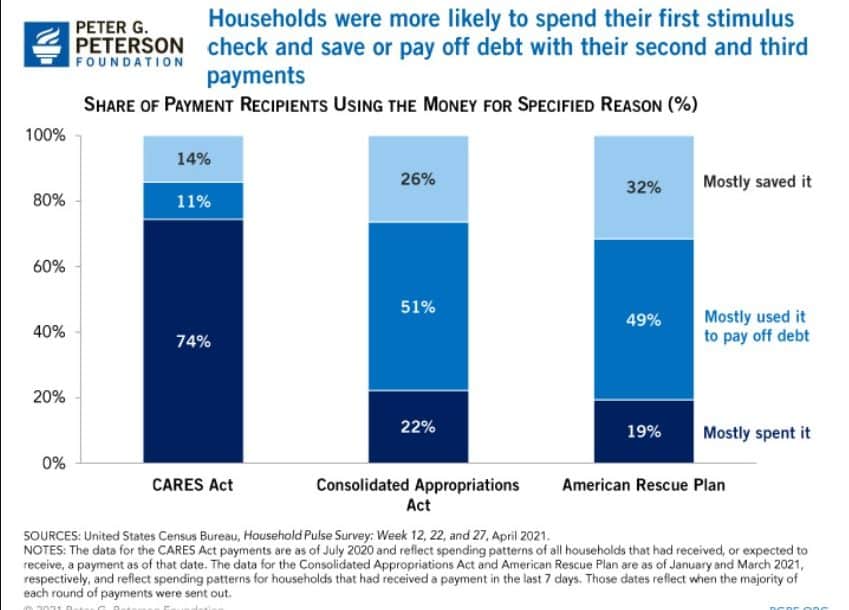

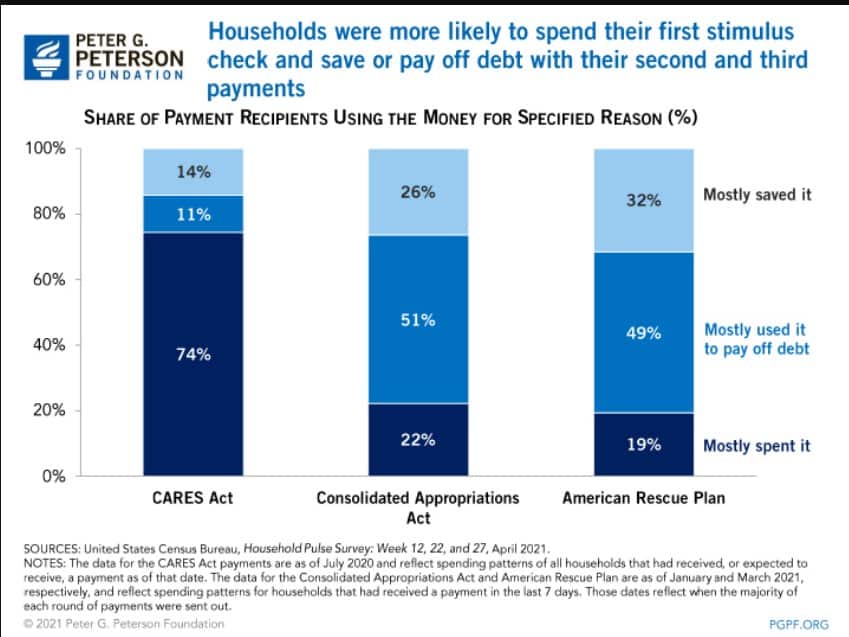

The spikes correlated with the federal stimulus payments. After the first round was distributed in April 2020, 14% of households saved most of the money. After the second round in January, 26% saved it. In March, 32% of families saved most of the stimulus money.

A Peter G. Peterson Foundation study showed that Americans shifted from spending the stimulus payments to paying down debt and saving.

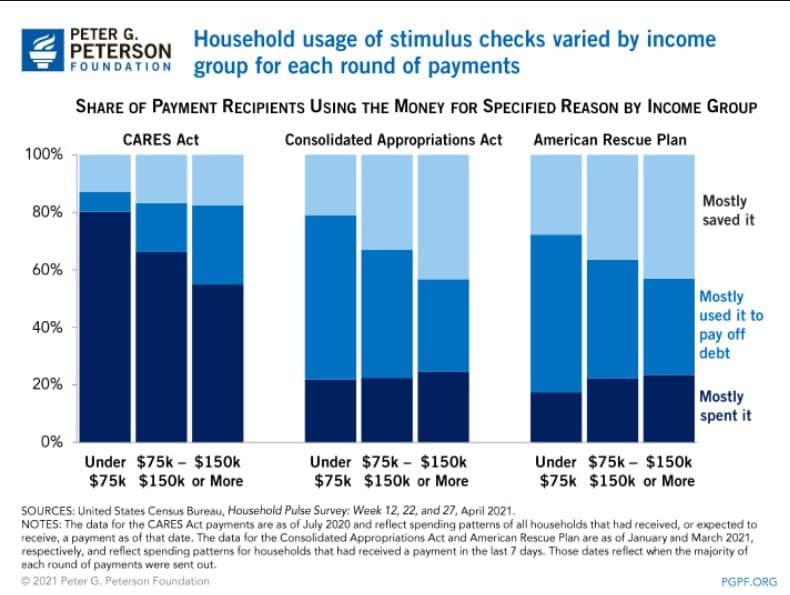

The study also found that although the majority of people in the lowest income group spent the first stimulus payment, that group shifted to the lowest spending cohort and paid down debt instead.

Another report shows that the savings habit is going beyond stashing stimulus cash. Voya Financial research found that consumers are shifting their mindset.

In the second quarter, 72% of Voya plan participants increased their contributions. A Voya survey also found that that more than half (63%) of Americans agree the pandemic has made them more focused on planning for retirement and 72% of Americans agreed they have become more of a “saver” and not a “spender.”

Heather Lavallee, CEO of Voya’s Wealth Solutions, said the data is encouraging, although there is still much to do in saving for retirement. But the generational spread in the new appreciation for saving is a good sign.

“We’ve seen this increase in retirement savings across all generations,” Lavallee said. “And while it’s not surprising to see baby boomers and Generation X saving more — as they may be earning more than younger generations — the pandemic has clearly made saving for the future a priority among all generations as both millennials and Generation Z are also saving more. Finding that retirement remains a priority amid this uncertainty provides a promising outlook, and that is good news.”

She tempered that sentiment with a caution about the return to some semblance of normal.

“As the economy returns to ‘normal’ and individuals are provided with more opportunity for discretionary spending, prioritizing saving over spending is going to remain a critical component for future success,” Lavallee said. “We can’t lose sight of the importance of saving for retirement, and employers should help support this momentum.”

The St. Louis Fed report bears out Lavallee’s caution in that the lower income groups have not been able to sustain their savings rate.

“Low-income households have been disproportionately affected by financial hardship during the pandemic, and many of those households have had to either draw on savings or go into debt, which is not reflected in the aggregate personal saving rate,” according to a Federal Reserved Economic Data blog post. “Moreover, these households were already less likely to be able to save. According to Survey of Consumer Finances data from 2019, about 37% of families in the lowest quintile of the income distribution reported saving some portion of their income over the previous 12 months. About 86% of families in the highest decile of the income distribution reported doing so.”

Steven A. Morelli is a contributing editor for InsuranceNewsNet. He has more than 25 years of experience as a reporter and editor for newspapers and magazines. He was also vice president of communications for an insurance agents’ association. Steve can be reached at [email protected].

© Entire contents copyright 2021 by InsuranceNewsNet. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.

Idaho Posts Preliminary Health Insurance Premium Rates

NLPC Blasts Board Diversity Rule

Advisor News

- Worker retirement confidence dips to lowest level in a decade

- What’s behind private equity investment in insurance brokerages

- Advisors get a win as NJ Senate passes independent contractor bill

- Why federal retirement benefits are more complex than advisors realize

- Why timing the market is still a retirement mistake and what to do instead

More Advisor NewsAnnuity News

- Best’s Special Report: U.S. Life/Annuity Industry Sees Bottom-Line Growth Despite 18% Decline in Total Income in First-Quarter 2026

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- Fortitude Re Completes $500 Million FABN Issuance

- Reframing retirement income for greater certainty

- Jackson Introduces Dow Jones Industrial Average Index Option, Flexible Premiums, Six-Year Rate Guarantee in Latest Registered Index-Linked Annuity Launch

More Annuity NewsHealth/Employee Benefits News

- Findings from Brown University Provides New Data on Managed Care (Low-Value Care Following Hospital and Private Equity Acquisition in Primary Care): Managed Care

- Reports from University of Chicago Medicine Advance Knowledge in HIV/AIDS (A Community Located Insurance Navigation Intervention to Link Sexual and Gender Minorities in Status Neutral Care: Results From the Navigating Insurance Coverage …): Immune System Diseases and Conditions – HIV/AIDS

- New Insurance Findings from Johns Hopkins University Outlined (Medicare coverage choice is not neutral: how policy design shapes beneficiary enrollment): Insurance

- Collinsville man, St. Louis woman charged in Illinois health fraud case

- Governor vetoes changes to health-care risk pool oversight

More Health/Employee Benefits NewsLife Insurance News

- Researchers from Georgia Institute of Technology Report on Findings in Insurance (Black Life Insurance Companies, Mortgages, and African American Homeownership Before 1964): Insurance

- How much money do Connecticut residents need to retire comfortably?

- Earl Dudley Jr. to Become Chief Human Resources Officer at Mutual of Omaha

- How accelerated underwriting is transforming life insurance

- OVER $107 MILLION IN LIFE INSURANCE BENEFITS LOCATED FOR TENNESSEANS IN 2025 THROUGH NAIC'S LIFE INSURANCE POLICY LOCATOR SERVICE

More Life Insurance News