Rise in Shorter-Term Surrender FIAs Means Commission Declines

The emerging popularity of fixed indexed annuities (FIA) with a seven-year surrender period is reducing commission income to agents, data shows.

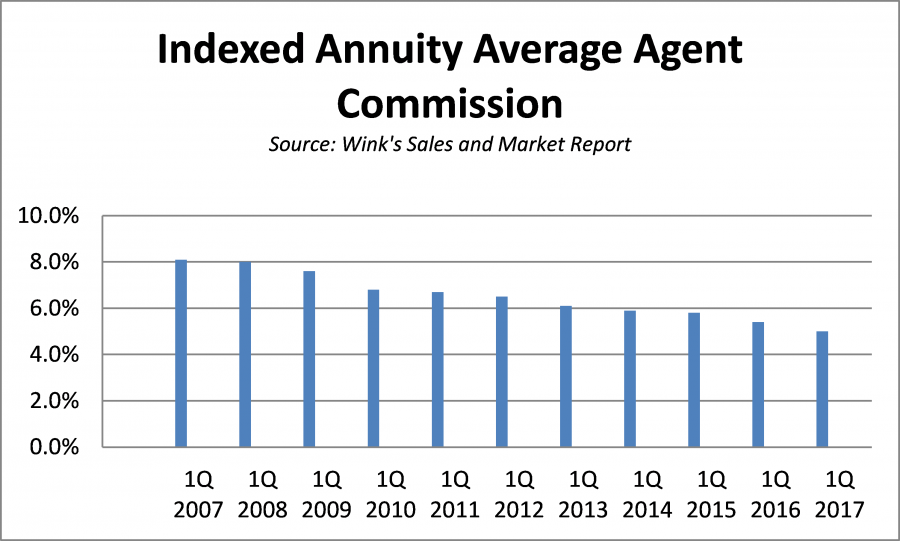

First-quarter indexed annuity commission received by agents dropped to 4.96 percent from 5.37 percent in the year-ago period, data from Wink’s Sales & Market Report indicate.

“Shorter-term products pay lower commissions,” said Sheryl J. Moore, president and CEO of Moore Market Intelligence and Wink, publisher of the life and annuity industry data tracker Wink’s Sales & Market Report.

“Agents are obviously having to work just as hard as they did last quarter, to make even less money,” she said.

At Quinlan Insurance & Financial Services in Winona, Minn., the most popular FIAs are the ones with seven-year surrender schedules, which means the commissions probably won’t be as high as those with 10-year surrender schedules.

“Shorter term surrender charge products are in our future, whether it's fixed, indexed or variable, that’s what I’ve heard,” said owner Bob Quinlan.

7-Year FIA’s Show Strong Sales

Surrender charges penalize an annuity contract holder for canceling the contract before a certain date, and allow insurance companies to recoup their commissions paid upfront to advisors on the sale of a commission-based contract.

Charges are typically pegged to a sliding scale with higher charges in the earlier years and lower charges in the later years before disappearing altogether.

Some surrender charges on FIAs can be as short as four years, while other surrender charges can go out as far as 15 years or more.

First-quarter sales of FIAs with a seven-year surrender period made up 22.1 percent of FIA sales, data shows.

In the first quarter 2016, sales of FIAs with a seven-year surrender period made up 17 percent of all sales.

In the first quarter this year, 42.8 percent of all FIA sales were for products with a surrender period of less than 10 years. Last year, first-quarter sales of FIAs with surrender periods of less than 10 years came to 36.8 percent of all FIA sales.

Fiduciary Rule Indirectly Implicated

Companies have been rolling out annuity products with shorter surrender periods for more than a year.

Releasing more short-term surrender products is a byproduct of the Department of Labor’s fiduciary rule, the first phase of which kicked in June 9.

The rule, which raises investment advice standards, encourages agents to move away from selling FIAs with long surrender charge periods.

But the new rule isn’t the only reason for the shift toward shorter surrender periods.

“Banks and broker-dealers typically sell shorter-term annuities and this quarter those channels captured 37.1 percent of all sales,” Moore said.

Banks and broker-dealers, which are considered financial institutions under the fiduciary rule, captured 32.2 percent of FIA sales in the fourth quarter of last year.

Forty percent of indexed annuity products in the top 10 for overall sales in the first quarter of the year were seven-year surrender charge products. Traditionally, the top 10 is usually dominated by FIAs with surrender charges of 10 years or more.

“This is significant,” Moore said.

InsuranceNewsNet Senior Writer Cyril Tuohy has covered the financial services industry for more than 15 years. Cyril may be reached at [email protected].

© Entire contents copyright 2017 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

What Advisors Need to Know About the Military’s New Retirement System

Direct Mail: An Important Ingredient In Your Marketing Mix

Advisor News

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Walla Walla residents drop health insurance because of affordability under Trump

- New Life Science Study Findings Recently Were Reported by Researchers at Johns Hopkins University Bloomberg School of Public Health (Formulary-Related Insurance Denials of Single-Source Branded Drugs in the United States): Life Science

- Trademark Application for “MEMORIAL HERMANN HEALTH PLAN MEDICARE ADVANTAGE PLANS HEALTH PLAN COMMERCIAL GROUPS” Filed by Memorial Hermann Health System: Memorial Hermann Health System

- Harrison: Rising health insurance exchange costs bad news for working poor in MS

- 94% of Americans say Congress must act on health care costs

More Health/Employee Benefits NewsLife Insurance News

- How can more Americans achieve financial independence?

- AM Best Assigns Credit Ratings to MAAGAP Insurance Inc.

- Critical care riders: the living benefit more clients should understand

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

More Life Insurance News