Indexed, MYGA annuities set Q1 sales record, says Wink

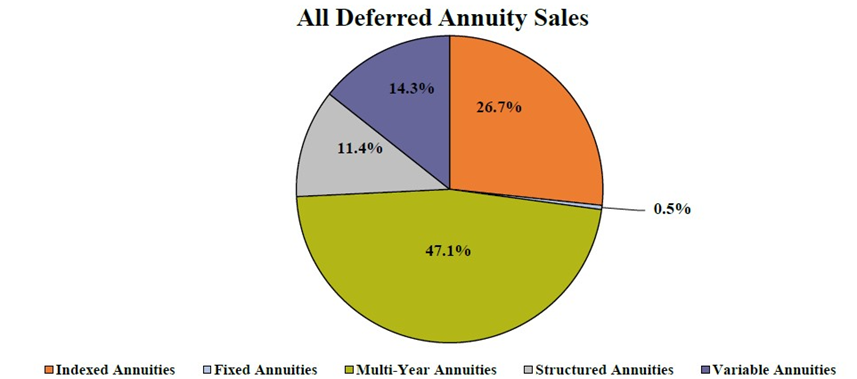

Annuity sales are on a hot streak. In fact, indexed and multi-year guaranteed annuities set an all-time sales record in the first quarter of 2023, with deferred annuity sales at $84.7 billion, up 6.8% compared to the previous quarter, and up a whopping 41.9% compared to the same period last year. Deferred annuities include the variable annuity, structured annuity, indexed annuity, traditional fixed annuity, and multi-year guaranteed annuity product lines.

Those numbers, compiled by Wink Inc.’s sales and market report, put Athene USA as the number one carrier overall for deferred annuity sales, with a market share of 10.2%. Corebridge Financial was second, while Massachusetts Mutual Life Companies, New York Life, and Allianz Life rounding out the top five carriers in the market. Athene’s MYG 5, was the top selling deferred annuity for all channels combined in overall sales.

The one lagging product was variable annuities, which recorded flat sales in the first quarter and were down more than 34% from a year ago.

“I just keep saying this,” said Sheryl Moore, CEO of both Wink, Inc., and Moore Market Intelligence. “Variable annuity sales likely have never been lower. Until the market turns around, the sales declines will continue.”

Wink’s numbers pretty much track those of LIMRA’s Individual Annuity Sales Survey earlier this month, which pegged total first quarter annuity sales at $92.9 billion, a 47% increase from the prior year. This would represent the highest quarterly sales ever recorded, according to LIMRA’s preliminary results. LIMRA predicts total annuity sales will top $300 billion in 2023 for the second consecutive year.

A perfect storm of faltering stocks and bonds, fears of recession, inflation, and rising interest rates has investors running to what they see as safer havens of annuities, which can offer guaranteed income streams.

“In ugly times, people get concerned about safety,” said Lee Baker, a certified financial planner and founder of Apex Financial Services, based in Atlanta, and a member of the Consumer News and Business Channel’s (CNBC) Advisor Council.

While there are many types of annuities, they mostly belong to two categories of investment or quasi-pension plan offerings. Issued by insurance companies, they provide a hedge against wildly swinging markets or the chances one might expend all their savings in retirement.

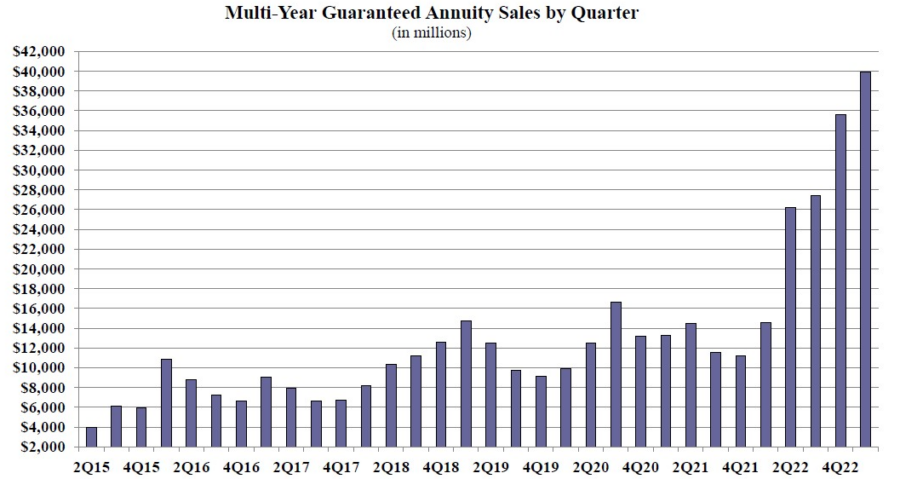

The single biggest sales of annuity products was in the multi-year guaranteed annuity (MYGA) category, which recorded sales of nearly $40 billion in the first quarter, according to Wink, an increase of 12% compared to the previous quarter, and up 173% compared to the first quarter last year. MYGAs have a fixed rate guaranteed for more than one year. The first quarter marked the greatest MYGA sales have been since Wink started tracking sales of the products in 2015.

“As long as CD rates remain so low, relative to annuity rates, you can count on indexed and MYG annuity sales being high,” said Moore.

Indexed annuity sales for the first quarter were $22.6 billion; up 4.4% when compared to the previous quarter, and up 35.5% when compared with the same period last year. Indexed annuities have a floor of no less than zero percent and limited excess interest that is determined by the performance of external indices, such as the Standard and Poor’s 500.

While increasingly popular, annuities aren’t right for everyone, financial mangers caution. For one thing, the older one is when they contract the annuity, the higher the rates will be compared to one purchased at a younger age. They also lack some flexibility as they are locked in at time of purchase and cannot be moved to take advantage of rising interest rates. Financial planners also note that situations change while annuity rates are fixed and cannot be adjusted for changing income needs. Annuity income is also taxed at marginal rates of 22% to 35% for middle-income households.

“Higher interest rates have made annuities an attractive option for investors since they offer a steady and secure source of income over time, making them especially appealing to baby boomers retiring today who are looking to supplement their fixed sources of income,” Eric Hutter a financial professional and host of the Eric Hutter Safe Money And Income Radio Show, told annuities.com. “Additionally, with more and more baby boomers reaching retirement age every day, there is a continual need for investments that can provide long-term security. These elements have come together to drive record-high fixed annuity sales and propel total annuity sales beyond what was once thought possible.”

Doug Bailey is a journalist and freelance writer who lives outside of Boston. He can be reached at [email protected].

© Entire contents copyright 2023 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Empowering African American agents to remain in the game

Unlocking the power of FIAs in a secure retirement plan

Advisor News

- Family communication: Financial planning’s growing blind spot

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

More Advisor NewsAnnuity News

- Investigation finds deceptive sales, churning of annuities targeting postal workers

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

More Annuity NewsHealth/Employee Benefits News

- CareScout Redefines Worksite Long-Term Care Insurance With a Solution That Goes Further for Employers and Employees

- Next Generation My Care – It’s here … now what?

- 4 common LTC missteps older Americans must avoid

- Missouri and Kansas can expect double-digit Obamacare premium hikes again

- Teachers and other state employees brace for possible health insurance increase

More Health/Employee Benefits NewsLife Insurance News

- The silver economy ushers in a new era of life insurance growth

- Family communication: Financial planning’s growing blind spot

- Indiana eyes more oversight of insurance companies' exposure to private credit

- HEALEY-DRISCOLL ADMINISTRATION RETURNS $14.5 MILLION TO HEALTH AND DENTAL INSURANCE CONSUMERS AND BUSINESSES

- ‘Uniquely positioned’: Equitable outlines future post-Corebridge merger

More Life Insurance News