Beyond the S&P 500: The case for RILA diversification

For many financial professionals, the S&P 500 has become the default choice when investing client funds in registered index-linked annuities (RILAs).

New data from Equitable reveals that diversifying into less understood or potentially more volatile asset classes, like small-caps or emerging markets, can pay off as well.

While the S&P 500 offers broad, large-cap U.S. exposure, it does not capture all market segments or international opportunities. Adding indices like the following may introduce sources of return that behave differently over time, the new data found.

• Small-cap U.S. stocks (Russell 2000®) expand diversification further by capturing companies earlier in their growth cycle, which often behave differently than large, established firms and can provide higher long-term return potential.

• International stocks (MSCI EAFE) introduce exposure to faster-growing regions, different currencies and markets that may perform well when the U.S. lags.

• The NASDAQ 100® adds more emphasis on innovation-driven and technology-oriented companies, which may follow distinct performance cycles.

“By blending these indices, financial professionals can help clients tap into a range of growth themes and reduce the portfolio's sensitivity to sector or geographic weakness,” said Dr. Wade Pfau, professor of retirement income at The American College of Financial Services, and author of the research.

Many annuity providers rely on the S&P 500 because it has performed well in recent years, explained Pete Golden, chief sales and distribution officer for Individual Retirement at Equitable. He noted, however, that while the S&P looks great in the past, no one can predict what it will look like in the future.

“We see a heavy reliance on the S&P 500 being the primary source for most fixed index annuities and RILAs,” Golden said. “Diversifying with other indexes may create better outcomes.”

Since RILAs have had strong growth over the past five years, he said, there is increasing interest among financial professionals about how they can assist their clients using these products.

According to LIMRA’s U.S. Individual Annuity Sales Survey, RILA sales set new quarterly and annual sales records in 2025. In the fourth quarter of 2025, RILA sales were $22.1 billion. For the full year, RILA sales increased 20% year over year to $79.5 billion –10 times the sales recorded a decade ago for this product line.

A historical case for diversification

The Equitable research looked back over 20 years of historical performance, and found that a diversified portfolio, which includes a 40% investment in an S&P 500 segment, significantly outperforms a portfolio that is only allocated to an S&P 500 segment.

After 20 years, a diversified portfolio has a 31% greater account value, providing significant value over a non-diversified portfolio.

Looking back over time, different indices come out ahead. What performs well in one cycle can lag in another.

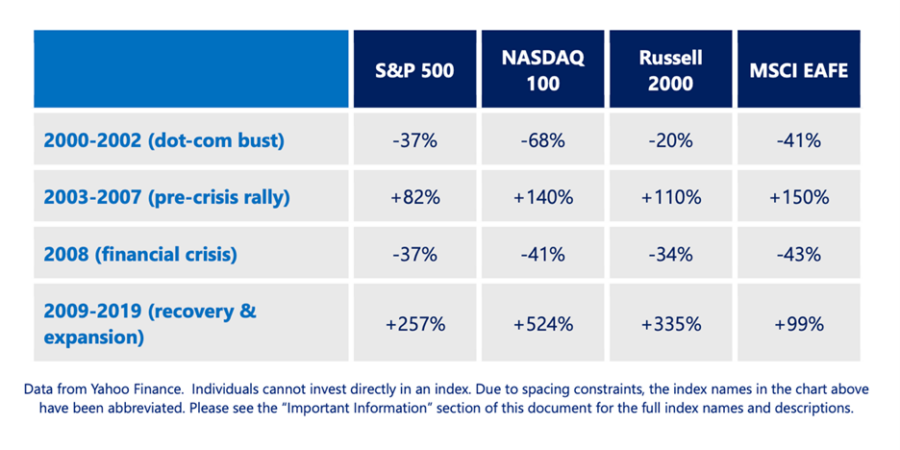

Returns from investments in other indices can surpass or pace the S&P 500. Data from 2009-2019 demonstrates the returns from each index below:

• S&P 500: +257%

• NASDAQ 100: +524%

• Russell 300: +335%

• MSCI EAFE: +99%

“Taking a diversified approach reduces exposure to any single market and offers downside protection, especially during periods when large-cap U.S. stocks underperform,” Pfau said.

While the research tested a specific Equitable product – the Structured Capital Strategies Premier (SCS Premier), a tax-deferred RILA – Golden noted that most index-based annuities provide access to multiple indices.

“Clients can be prepared for all market conditions regardless of the index with a broad range of crediting strategies and buffers,” he said.

With the SCS Premier, clients can use segments such as Dual Direction, which can deliver positive returns even when the market is down, or they can use deeper buffers up to 40% to protect against volatile markets. Additionally, clients are not locked into their segments until maturity; if financial professionals believe market conditions are shifting, they can easily reallocate clients into new segments at any time.

“Broader diversification within annuity segments offers the potential to improve the risk/return trade-offs for client portfolios,” Pfau said. “By thoughtfully adding complementary indices, different crediting strategies, and deeper buffers, financial professionals can help clients potentially have a smoother ride along the journey to meet their financial goals.”

“In today's markets, helping your clients widen their range of indices may be a strategic move that could potentially help them meet their long-term financial objectives and better set the stage for retirees to face their futures with confidence,” Golden added.

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Rethinking the ways employers manage benefits risk

Retirement is increasingly defined by a secure income stream

Advisor News

- Embracing a family-centric approach to financial planning

- Family communication: Financial planning’s growing blind spot

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

More Advisor NewsAnnuity News

- Investigation finds deceptive sales, churning of annuities targeting postal workers

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

More Annuity NewsHealth/Employee Benefits News

- Louisiana hospitals see sharp uptick in uninsured patients after Obamacare subsidies expired

- Louisiana hospitals see sharp uptick in uninsured patients after Obamacare subsidies expired

- CareScout Redefines Worksite Long-Term Care Insurance With a Solution That Goes Further for Employers and Employees

- Next Generation My Care – It’s here … now what?

- 4 common LTC missteps older Americans must avoid

More Health/Employee Benefits NewsLife Insurance News

- Built to Last: Winston-Salem—a quiet industrial powerhouse

- The silver economy ushers in a new era of life insurance growth

- Family communication: Financial planning’s growing blind spot

- Indiana eyes more oversight of insurance companies' exposure to private credit

- HEALEY-DRISCOLL ADMINISTRATION RETURNS $14.5 MILLION TO HEALTH AND DENTAL INSURANCE CONSUMERS AND BUSINESSES

More Life Insurance News