Rising Interest Rates Scramble Annuity Sales Forecasts

Annuity exchanges could become big business over the coming quarters as short-term fixed-rate deferred contracts expire.

It is part of a business climate supercharged by the rise in interest rates, said Todd Giesing, assistant vice president, Secure Retirement Institute Annuity Research.

"The pace of change is just unbelievable and trying to keep up with it is a challenge for the insurers," he said. "But it's also an opportunity."

Giesing will be joined by Teddy Panaitisor, research analyst for SRI, for a session today titled, "Bringing it all Together: Annuity Market Overview & Redefining the Future" at the Retirement Industry Conference, hosted by SRI and the Society of Actuaries.

The 10-year Treasury rate began 2022 at a measly 1.5% and climbed to 3.1% as of Friday. The Federal Reserve hiked short-term interest rates by 0.50% last week, as part of an effort to tamp down the inflationary pressures weighing on Americans.

It all adds up to a nice runway for annuity sales, Giesing said. While first-quarter sales tend to lag, March saw record-high numbers, the SRI reported last week. Total 1Q annuity sales increased 4% to $63.6 billion, a lot of it coming after an initial 0.25% rate hike by the Fed in March.

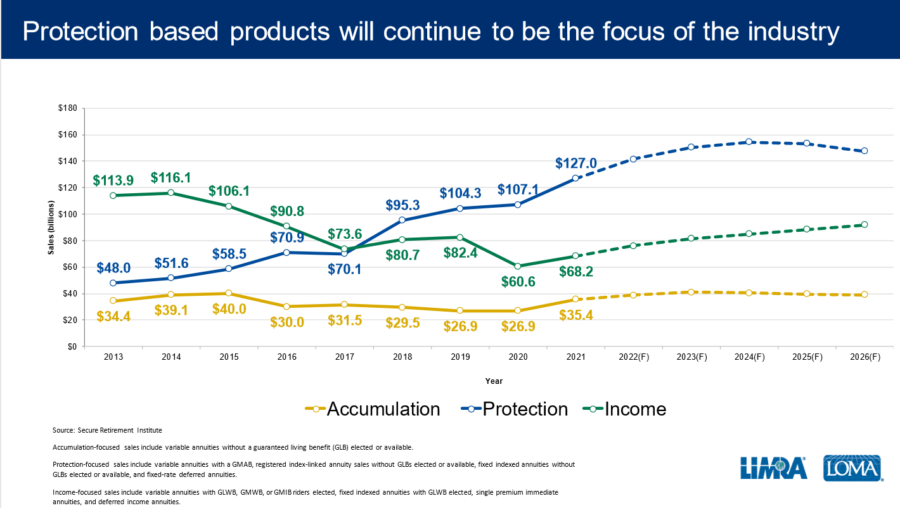

“Rising interest rates and increased market volatility shifted the product mix this quarter with fixed annuity products driving the overall growth," Geising said.

Total fixed annuity sales were $35.2 billion, up 14% over first quarter 2021. Double-digit growth for fixed indexed annuities and fixed-rate deferred annuities drove the overall fixed annuity sales to pre-pandemic levels.

Exchanges Could Be Coming

Annuity exchanges are a likely source of money in the coming quarters, Geising said, adding that SRI has no data on the market. But ultra-low interest rates led to many very short contracts for fixed-rate deferred annuities in recent years.

"Our assumption is most of these contracts are short duration, three years, maybe five years tops, just because of the way the rate environment has been over the past two years," Geising explained. "It just doesn't pay to go long on the duration. There's just not enough extra crediting in the longer ones because of the way rates have fallen over the past few years."

When those contracts come due, the money has to go somewhere, he added.

"We do expect that there'll be a cycle of money in motion that will continue to feed fixed-rate deferred sales for the next couple of years," Giesing said.

A RILA Sales Blip?

The recent annuity sales star, registered index-linked annuities, receded a bit in the first quarter. RILA sales were $9.3 billion, 2% higher than first quarter 2021, but a 10% drop from prior quarter. RILA products still have plenty going for them, Giesing said, calling the sales dip "a momentary blip."

Projections for equity markets are not promising over the next five years, he noted, which makes the downside protection offered by RILAs more attractive.

"The other factor we're watching very closely is the rise of guaranteed living benefits in this segment," Giesing said. "We feel there's potential from the RILA market for guaranteed living benefits to be a larger component."

InsuranceNewsNet Senior Editor John Hilton has covered business and other beats in more than 20 years of daily journalism. John may be reached at [email protected]. Follow him on Twitter @INNJohnH.

© Entire contents copyright 2022 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Advisor News

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Harrison: Rising health insurance exchange costs bad news for working poor in MS

- 94% of Americans say Congress must act on health care costs

- They harvest the nation’s food, but a new rule may strip them of health insurance

- NEW DATA SHOWS 5 MILLION AMERICANS LOST HEALTHCARE THANKS TO GARRITY-BACKED CUTS

- Get Your Kids Ready to Go Back-to-School with Affordable Health Coverage

More Health/Employee Benefits NewsLife Insurance News

- How can more Americans achieve financial independence?

- AM Best Assigns Credit Ratings to MAAGAP Insurance Inc.

- Critical care riders: the living benefit more clients should understand

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

More Life Insurance News