Using life insurance in a cash balance plan

Let’s look at why some cash balance plan sponsors allocate a limited portion of plan assets to permanent life insurance for stability, funding efficiency and risk management, when done within the qualified plan rules and a prudent fiduciary process.

Why it matters

The problem sponsors feel is volatility equals contribution surprises. Cash balance plans are defined benefit plans maintained under Internal Revenue Code §401(a), in which the plan sponsor ultimately bears funding responsibility for promised benefits. When markets drop, funded status can decline and contributions can become unpredictable, often when business cash flow is already under pressure. Employee Retirement Income Security Act fiduciary standards evaluate investments in the context of the plan portfolio, including diversification, liquidity relative to cash‑flow needs and return relative to funding objectives.

The strategy: Adding a stabilizing plan asset

Treasury department regulations recognize that qualified pension plans may provide incidental death benefits through insurance or otherwise, as long as the plan primarily remains retirement‑oriented. In that context, some sponsors consider a limited allocation to permanent life insurance owned by the plan trust, positioned as a risk‑managed funding asset rather than a retail accumulation product.

The value proposition

For the plan sponsor (usually the business owner):

» Smoother funded status equals fewer surprise contributions when markets decline (prudence considers liquidity and funding objectives at the portfolio level).

» Stability for outcomes equals lower‑

volatility assets that may better align with liability growth than equity‑heavy allocations do (asset/liability driven methodology).

» If an insured participant dies preretirement, death benefit proceeds received by the plan may help settle plan obligations (subject to incidental benefit limits and plan terms). A portion of the proceeds is received income tax-free to the beneficiary, provided the economic benefit has been reported and paid.

For the advisor:

» Differentiates your cash balance strategy as outcome‑driven by managing volatility, managing funding and managing the fiduciary process.

» Creates a repeatable process: design plan, document, orchestrate, implement and monitor.

How it works

Let’s examine a numeric funding example. This example is illustrative, not product specific.

Your client is a 55‑year‑old owner of a professional practice. Their goal is larger deductible contributions with controlled volatility, and the plan provides pay credits and an interest‑crediting formula.

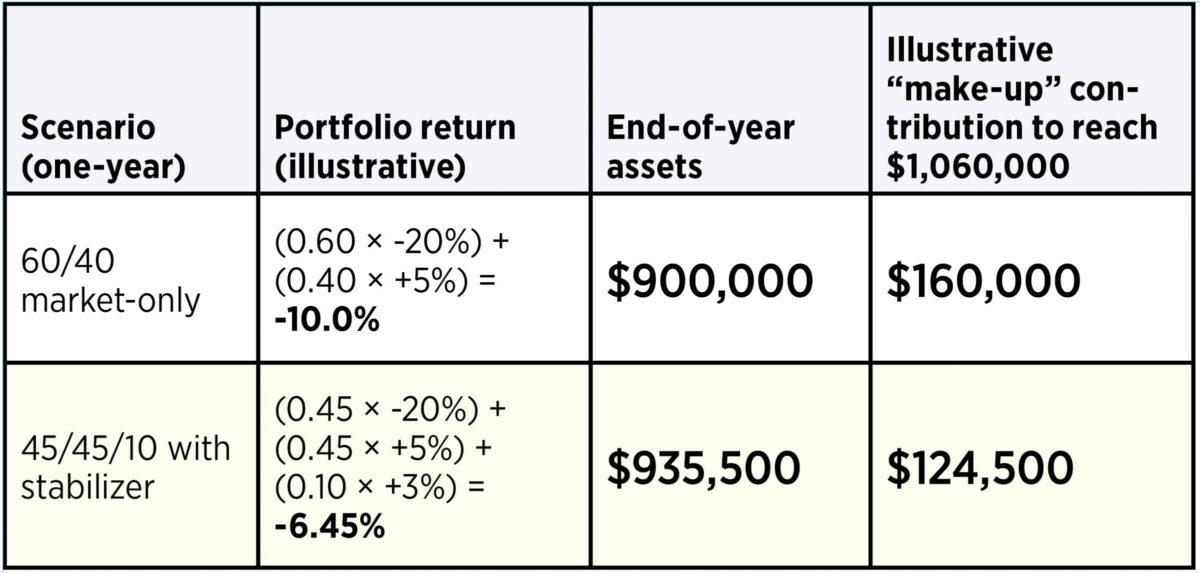

Two portfolio approaches (illustrative):

1. Market‑only: 60/40 (equity/bonds)

2. With stabilizing sleeve: 45/45/10 (equity/bonds/plan‑owned permanent life insurance cash value)

Assumptions (illustrative):

1. Beginning plan assets: $1,000,000

2. Target end‑of‑year assets (to stay on track with liabilities): $1,060,000 (approximately 6% objective for illustration)

3. Year market shock: equities ‑20%, bonds +5%

4. Insurance sleeve return shown as +3% (illustrative of smoother crediting; not guaranteed and not reflective of any product or carrier)

Illustrative funding impact (how advisors should frame it):

In this simplified illustration (see opposite page), adding a stabilizing sleeve reduces the “make‑up” contribution after a down year by $35,500. ERISA’s investment duties emphasize evaluating investments in context — especially liquidity and cash‑flow needs and the portfolio’s return relative to the plan’s funding objectives.

It’s important to note that this example is educational only. It is not an actuarial funding calculation, not a prediction and not a guarantee. Actual required contributions depend on plan provisions, funding methods and assumptions, timing, demographics, and current law.

Other points to note: The plan must meet various nondiscrimination tests, treating the life insurance availability and terms as a plan feature subject to nondiscrimination considerations. IRS guidance addresses issues where policy features or purchase rights differ across groups.

The goal is to achieve policy valuation, distribution and prohibited transaction controls. If policies are sold or distributed, there are valuation and transaction requirements and prohibited transaction compliance as applicable.

Cash balance plans are powerful, but volatility can drive unpredictable contributions. ERISA focuses on prudence at the portfolio level, diversification, liquidity and meeting funding objectives. A properly limited, plan‑owned life insurance allocation can add stability and, in the event of premature death, help self‑complete benefits, while staying within incidental benefit rules.

How annuities can help small-business owners achieve retirement security

What to do when term life runs out

Advisor News

- Financial shocks, caregiving gaps and inflation pressures persist

- Americans unprepared for increased longevity

- More investors will seek comprehensive financial planning

- Midlife planning for women: why it matters and how advisors should adapt

- Tax anxiety is real, although few have a plan to address it

More Advisor NewsAnnuity News

- LIMRA: Annuity sales notch 10th consecutive $100B+ quarter

- AIG to sell remaining shares in Corebridge Financial

- Corebridge Financial, Equitable Holdings post Q1 earnings as merger looms

- AM Best Assigns Credit Ratings to Calix Re Limited

- Transamerica introduces new RILA with optional income features

More Annuity NewsHealth/Employee Benefits News

- Southwest Washington leads state in premiums for qualified health plans and Medicaid

- Researchers at Golestan University of Medical Sciences Detail Findings in Managed Care (Shifts in Medicare Reimbursement for Common Lower Extremity Orthopaedic Trauma Procedures, 2006-2024): Managed Care

- NC House lawmakers push for better breast cancer detection

- Lincoln County Commissioners Review Insurance Increase, Approve Road Equipment Purchases

- All about AHCCCS: Navigating Arizona Medicaid's changing landscape

More Health/Employee Benefits NewsLife Insurance News

- Financial Focus : Keep your beneficiary choices up to date

- Equitable-Corebridge merger casts shadow over life insurance earnings

- When an MEC is an effective planning tool

- Lincoln Financial Reports 2026 First Quarter Results

- Brighthouse Financial Announces First Quarter 2026 Results

More Life Insurance News