Using Retirement Income Forecasting to Position Annuities

Guaranteed annuities, and particularly those offering Guaranteed Lifetime Income Benefits (GLIB), are increasingly popular for both retirees and those nearing retirement. Unfortunately, many are being sold to clients without the benefit of an in-depth analysis of the client’s retirement income needs; this can result in not providing enough guaranteed income, or providing too much. Both are problematic.

· Providing Too Little Guaranteed Income: The function of the GLIB, like all financial tools, is to provide the client with the security that they will have sufficient retirement income to at least meet their basic needs in retirement. If too little of the total savings assets are dedicated to secure income, then the income security provided by the GLIB is insufficient, thus the tool is underutilized.

· Providing Too Much Guaranteed Income: Allocating the client’s retirement savings is a balance between the need for safety and guaranteed income and the need for potentially higher earnings to maintain liquid assets and produce additional income from risk-based assets. Because guaranteed annuities (including Fixed Indexed Annuities) will generally produce less cash value growth than risk-based assets, dedicating too much of the total savings assets to secure income can cause the liquid assets (non-annuity) to deplete too soon, thus the tool is over-utilized.

One of the core benefits of a GLIB is the ability to predict – with absolute precision – exactly how much income will be produced for a given amount of premium at a given point in the future (this is true only of GLIB that fully guarantee the growth of the income base; for more information please review the article titled Guaranteed Lifetime Income Benefits - Part 3: What’s Guaranteed?). In order to allow the client to take advantage of this unique aspect of GLIB, we must have an idea of how much income will be needed, and when.

There is a delicate and difficult balance between safety-based assets/income and risk-based assets/ income that ideally must be achieved for the client; the way to find this balance is with detailed retirement income forecasting.

Ignore the 4% Rule and All the Other Rules

When forecasting retirement income and determining asset allocation, it has been common to use “rules of thumb” such as the “4% Rule,” the “40%/60% Bonds/Equities Rule,” or the most ridiculous of them all, the “100 – Age Rule.” The problem with these “rules of thumb” is that they bear almost no semblance to the reality of most retirees as regards their retirement expenses and spending desires. For the 21st Century Retiree, these rules are as applicable as is the origin of the term “rule of thumb,” which dates to medieval times as a means of measurement in commerce.

Just as medieval ways of measurement no longer apply in the 21st Century, today’s typical retiree does not fit “the old model” around which these rules were developed; that is, the model that assumes upon retirement that the house is paid-for, that expenses are significantly reduced in retirement, and retirement income is a combination of Social Security, pension, and distributions from savings. As those of us continually engaged in retirement income planning know all-too-well, the typical “boomer” retiree of today has a mortgage for several years during retirement (or for the whole duration), and the expenses saved by no longer working are more than made-up-for by expenses related to hobbies, recreation, family assistance, and travel. Therefore, retirement income forecasting should be done based upon an analysis of the clients’ anticipated consumption needs and desires in retirement, and this varies greatly amongst individuals.

“Consumption-Based” Retirement Income Forecasting

As the term implies, “consumption-based” income forecasting begins with a focus upon what the client both needs and wants to spend during retirement; in other words what they will “consume.” While there are several legitimate “schools of thought” as regards method, this Author submits that the total spending (“total consumption”) should be categorized between expenses that are critical, and those that are less so.

· Critical Expenses: These are expenses in retirement that provide for basic comfort and needs, as defined by the individual client. For most retirees, these expenses include the mortgage payment and costs related to maintaining their primary residence such as utilities, important insurance premiums, food and clothing, transportation, and medical expenses. The client must know that the income to pay for critical expenses is reliable, sustainable, and predictable for the duration of their retirement, regardless of what is happening in the stock markets or economy.

· Non-Critical Expenses: These are retirement expenses that are discretionary, providing the things and activities that support a desired lifestyle, but are typically not critical to basic comfort. These include spending on things such as travel, dining-out, vacation residences, recreation, and entertainment. While predictability of the income to pay for non-critical expenses is certainly desired, that predictability is much less important than is that for critical expenses.

The process begins with forecasting both the critical and non-critical expenses. These expenses should be forecast with inflation for the anticipated duration of retirement, typically a forecast should be for at least 20 to 25 years. Speaking of inflation, take care not to overstate it. Ideally, different rates of inflation should be applied to different types of expenses, as some expenses don’t inflate, while other expenses inflate more than do others.

For example, a fixed-rate mortgage does not inflate, whereas medical expenses inflate at a higher rate than do cell phone costs. Similarly, the expense forecast should incorporate known or anticipated changes to major expenses, such as when a mortgage is paid-off, anticipated reductions in travel and activities as the client ages, and the potential for out-of-pocket medical costs to increase with age. The image at right is an example of applying different inflation rates to different expense; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process.

Only apply inflation to the expense, not the pre-tax income required to pay for the after-tax expense. Inflating the pre-tax income will skew the forecast future income upward, which can cause the client to believe they need to take more risk than perhaps they really need to. Inflating only the expenses, and then determining the pre-tax income needed to pay for those expenses will produce a more accurate picture of the income needed and desired at future points in time.

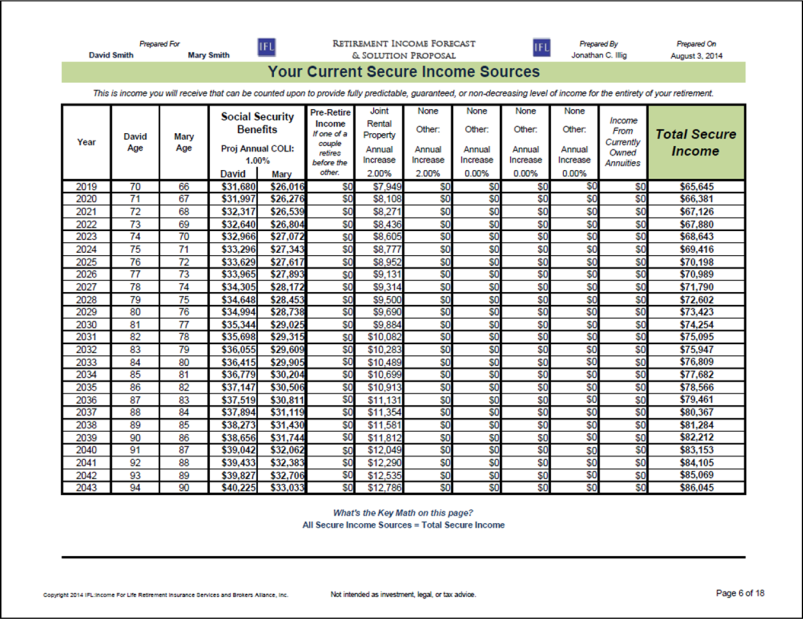

Next Compare to Secure Income. Once both critical and non-critical expenses, along with inflation projections, have been forecast and converted to the pre-tax income required to pay for those after-tax expenses for the retirement duration, we now have a picture of what future income needs and desires are. This can be a starting point for determining how best to use a GLIB, but more accuracy is really needed to determine how best to best utilize the GLIB tool. We must complete the picture by comparing the forecast income needs and desires to the “secure income sources” the client will have (or has) in retirement. Examples of “secure income sources” are Social Security benefits, pensions, or in many cases rental property or business income. Just as we forecast expenses with inflation, we must forecast these secure income sources with anticipated Cost of Living Increases (Social Security benefits) or other increases, if any (i.e. increases in rental property or business income over time). The image at right is an example of projected secure income sources over the retirement duration; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process.

Next Compare to Secure Income. Once both critical and non-critical expenses, along with inflation projections, have been forecast and converted to the pre-tax income required to pay for those after-tax expenses for the retirement duration, we now have a picture of what future income needs and desires are. This can be a starting point for determining how best to use a GLIB, but more accuracy is really needed to determine how best to best utilize the GLIB tool. We must complete the picture by comparing the forecast income needs and desires to the “secure income sources” the client will have (or has) in retirement. Examples of “secure income sources” are Social Security benefits, pensions, or in many cases rental property or business income. Just as we forecast expenses with inflation, we must forecast these secure income sources with anticipated Cost of Living Increases (Social Security benefits) or other increases, if any (i.e. increases in rental property or business income over time). The image at right is an example of projected secure income sources over the retirement duration; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process.

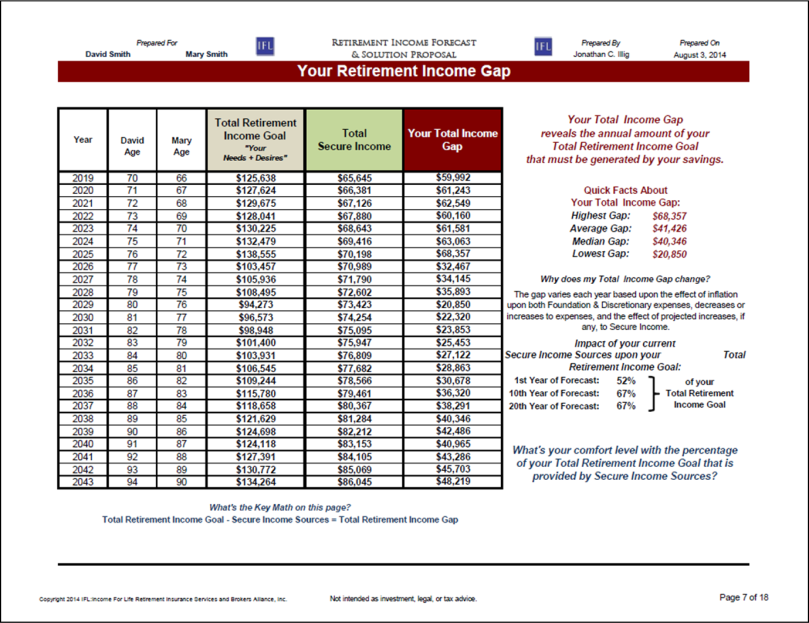

Now we can begin to properly position the annuity GLIB. “Consumption-based” analysis has now projected both the anticipated critical and non-critical expenses with inflation, but also the anticipated “secure income sources” that the client will receive during retirement. To properly position the annuity GLIB, the next step is compare the year-by-year expenses with the year-by-year secure income. This will show us and the client the year-by-year difference between the forecast income need, and their secure income sources; the year-by-year difference is their “income gap.”

Now we can begin to properly position the annuity GLIB. “Consumption-based” analysis has now projected both the anticipated critical and non-critical expenses with inflation, but also the anticipated “secure income sources” that the client will receive during retirement. To properly position the annuity GLIB, the next step is compare the year-by-year expenses with the year-by-year secure income. This will show us and the client the year-by-year difference between the forecast income need, and their secure income sources; the year-by-year difference is their “income gap.”

The “income gap” provides an initial logical basis upon which to determine how much income is needed from the annuity GLIB, and therefore the percentage of retirement savings to allocate to the annuity. The image at right is an example of projected “Total Income Gap” over the retirement duration; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process. Our process also drills-down even deeper to expose the clients’ “income gap” for both total income and the “income gap” for critical expenses.

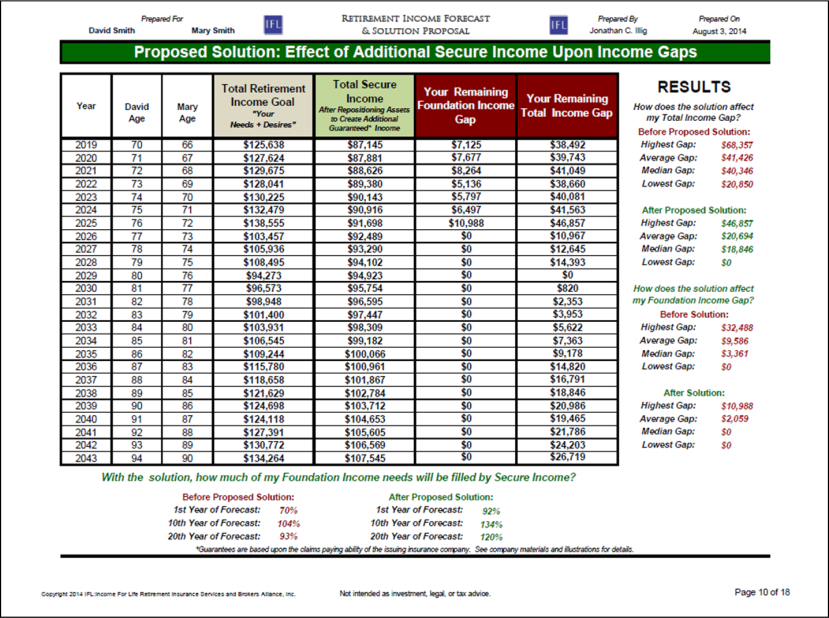

Refining the GLIB solution. Next, the financial professional must apply the GLIB solution (i.e. income and premium) to the picture to see how the additional secure income provided by the annuity GLIB will affect the “income gap,” and how the premium allocation will affect liquid assets over the retirement duration.

First, examine the effect upon the “income gap.” Does the GLIB income provide enough guaranteed income to significantly reduce the “income gap?” The application of GLIB should provide a meaningful increase in total secure income; if it does not, then it is questionable whether or not the liquidity restriction inherent in a deferred annuity is suitable; the benefit must be meaningful to the client. The image at right is an example of a projected GLIB solution effect upon both the critical and non-critical income gaps over the retirement duration; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process.

First, examine the effect upon the “income gap.” Does the GLIB income provide enough guaranteed income to significantly reduce the “income gap?” The application of GLIB should provide a meaningful increase in total secure income; if it does not, then it is questionable whether or not the liquidity restriction inherent in a deferred annuity is suitable; the benefit must be meaningful to the client. The image at right is an example of a projected GLIB solution effect upon both the critical and non-critical income gaps over the retirement duration; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process.

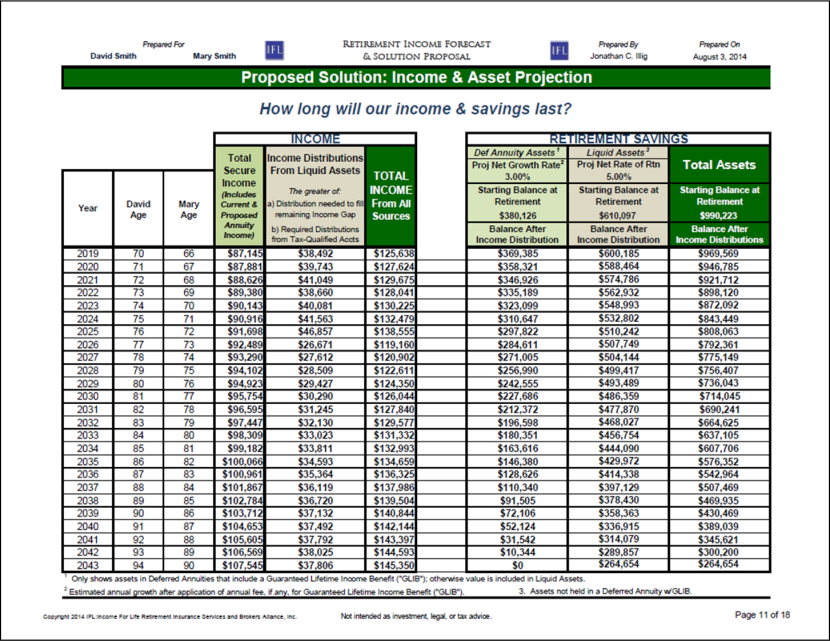

Finally, how does the allocation of premium to the annuity affect the sustainability of the other retirement savings assets? This is determined with an income and asset projection that includes the annuity solution. This provides a “test” to determine how long non-annuity assets, including additional income distributions from those assets, will last at a projected rate of return (be conservative). This helps to determine if the amount allocated to the annuity – with inherent lower cash value growth – is too much, resulting in liquid, non-annuity assets depleting too quickly in retirement. The image is an example of a projected GLIB solution effect upon the income and savings balances over the retirement duration; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process.

Finally, how does the allocation of premium to the annuity affect the sustainability of the other retirement savings assets? This is determined with an income and asset projection that includes the annuity solution. This provides a “test” to determine how long non-annuity assets, including additional income distributions from those assets, will last at a projected rate of return (be conservative). This helps to determine if the amount allocated to the annuity – with inherent lower cash value growth – is too much, resulting in liquid, non-annuity assets depleting too quickly in retirement. The image is an example of a projected GLIB solution effect upon the income and savings balances over the retirement duration; this is integral to the retirement forecasting process used in Brokers Alliance’ IFL Lifetime Income process.

In Closing. When integrating annuity GLIB solutions into our clients’ retirement plan, we must remember that we are dealing with their life savings, and it is in their best interests to take the time and effort to ensure that the solution we are proposing is well thought-out and meaningful to the client. We must take care to examine the pros and cons of the proposed annuity solution pertaining to both assets and income over the retirement duration. This is accomplished with “consumption-based” retirement income forecasting, which helps us ensure that the GLIB tool is neither over-utilized not under-utilized, but is properly utilized.

Jonathan C. Illig, Executive Sales Consultant at Brokers Alliance, is an 18 year veteran in annuity sales and support.

Jon may be reached at [email protected].

Brokers Alliance, Inc. has been serving the Brokerage Community in the areas of Life, Annuity, Retirement & Estate Planning, Long Term Care, and Disability Insurance for over 30 years. With 50+ employees, we are devoted to growing your business with superi-or Marketing Programs, Case Management, and Product expertise. Call Brokers Alliance at (800) 290-7226 or visit us at-www.brokersalliance.comk and how to explain them.

1Heart Caregiver Services Partners With Franchise Marketing Systems at West Coast Franchise Expo to Expand National Senior Care Franchise Program Strategically

Advisor News

- The overlooked retirement security risk that must be addressed

- What advisors should know about hedge funds in retirement planning

- Retirement control is top success measure for middle class, ACLI says

- Industry groups applaud House passage of Financial Exploitation Prevention Act

- Younger workers more likely to be eligible for a retirement plan after changing jobs

More Advisor NewsAnnuity News

- Malibu Life Holdings Completes Acquisition of TruSpire, Establishing Malibu USA and Accelerating Entry into the U.S. Retail Annuity Market

- Why job boards are failing insurance agencies

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

- What’s fueling record annuity growth?

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

More Annuity NewsHealth/Employee Benefits News

- Why More Sioux City Residents Choose Direct-Pay Dental Care

- Millions drop Affordable Care Act coverage amid price jump

- ICYMI: CLEVELAND.COM: TRUMP POLICIES HAVE COST OHIO HOUSEHOLDS THOUSANDS SINCE JANUARY 2025, REPORT FINDS

- 16K new moms to benefit from expanded Medicaid coverage

16,000 new moms to benefit from expanded Medicaid coverage starting Wednesday (Copy)

- REPUBLICANS' DISASTROUS HEALTH CARE AGENDA LEAVES MILLIONS OF AMERICANS WITHOUT COVERAGE

More Health/Employee Benefits NewsLife Insurance News

- NAIFA praises House committee approval of Clarity for Compensation Act

- PHL Variable liquidation pushed out to 2027, Connecticut regulators say

- ‘Recession-Proof’ Insurance Is Trending. Safety Net or Scam?

- Winged Keel Group Expands National Presence and PPLI Leadership, Welcomes SBSI, Inc. (dba NFP Insurance Solutions)

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

More Life Insurance News