Survey finds some support for DOL fiduciary rule

A new survey of financial professionals shows surprising and almost uniform support for the Department of Labor’s Retirement Security Rule that would require insurance brokers who provide retirement planning services be held to a fiduciary standard.

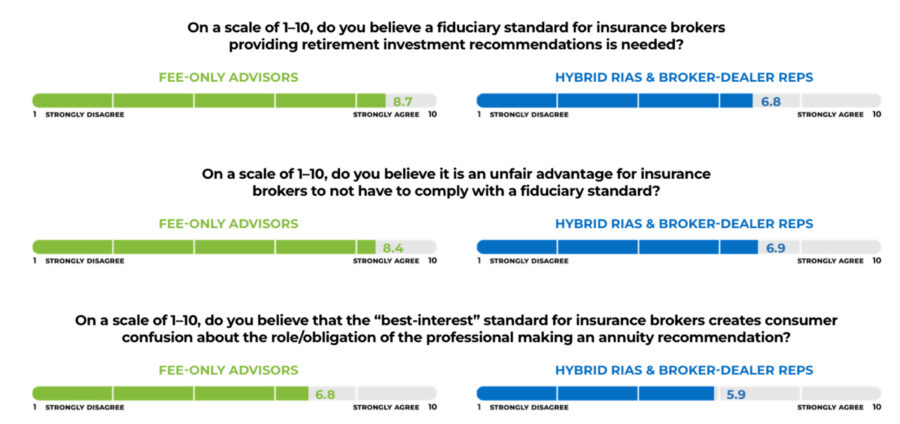

The survey of more than 230 advisors by DPL Financial Partners, fee-only advisors were more likely to strongly agree with the need for a fiduciary standard, but even hybrid RIAs and broker-dealer representatives were more likely than not to agree that a standard is needed.

“It’s remarkable to find such a strong consensus among all types of advisors that a fiduciary standard is needed when it comes to insurance products,” said DPL Founder and CEO David Lau. “The fact that hybrid RIAs and even broker-dealer reps, who receive compensation in the form of commissions, would welcome such a standard speaks volumes about the need for the Labor Department’s commonsense proposal.”

The DOL’s proposal, which was to go into effect in September, has been stayed by a pair of rulings in federal courts in Texas. The DOL has appealed. Considering strong opposition to the rule from the insurance industry, the advisors surveyed were uncertain it will survive, despite their strong agreement with it.

DPL recently hosted an online seminar titled “How Commissioned Annuities Fail Retirees,” in which participants generally agreed change was needed.

Panelist: Commissions at issue

“Annuities are always controversial and probably one of the most divisive financial products that are in the market, largely due to the commissions,” Lau said. “People who don't like commissions and don't accept commissions tend to think of annuities as a four-letter word. And people who like commissions tend to like annuities quite a lot because they pay very handsome commissions generally.”

Other panelists threw shade on the insurance industry’s major opposition to the DOL fiduciary rule that it would limit financial advice for everyday Americans.

“I've heard that argument before,” said Chuck Failla, founder, and CEO of Sovereign Financial Group. “But the argument is saying if you force a commission-based insurance salesperson to be a fiduciary, they can’t do their job. In my opinion, that's garbage.”

Failla said fears that the small investor will not get proper financial advice are unwarranted.

“What's going to happen is that agent is not going to be able to sell a $100,000 annuity with a 10% commission, walk away with $10,000 in commission, and never talk to that person again,” he said “That will stop. But that's not a bad thing in my opinion.”

A greater understanding for customers

Failla said the commissions would become planning fees and the customer would have a greater understanding of what, exactly, they are paying for.

“If you want to charge a fee for planning, charge a fee for planning,” he said. “And there are a lot of solutions now that are cropping up that are designed for that low net-worth person in which you can give a client advice that doesn't have to come via a $10,000 hit in commission.”

The panelists decried what they called PNOs (Planners in Name Only) and said the new fiduciary rule will bring more accountability and professionalism to the practice of financial advising.

“There is an absolute real culture and entire system dedicated to training those younger advisors,” Failla said. “They come in, they really don't know planning, but they go out with a pretense or being planners.”

Failla said typically these PNOs will ultimately recommend some variety of index universal life insurance policies for their clients.

“Why” he asked. “Is it the best for the client? Or is that the best way to bury an opaque, very high commission?”

Incentives cited

The panelists also noted an elevated level of incentives in the business for selling proprietary products that may or may not help customers. They cited reports of professionals winning lavish international travel, iPhones, and other goodies for hitting certain sales thresholds.

“This isn’t just about fees versus commissions or fiduciaries versus non-fiduciaries,” said Micah Hauptman, director of investor protection at The American College of Financial Services. “It's the differential compensation and all the other incentives that encourage and reward bad advice. If a financial professional could earn $5,000 for recommending and selling one annuity, but $10,000 for recommending and selling another, it's pretty clear that their incentive is to recommend the one that pays them $10,000, even if that annuity is worse for the investor. It’s human nature and not about bad people. It’s people responding to incentives.”

He said the financial products would better compete based on cost and quality, not how much they compensate the salesperson or the producer.

Despite some problematic issues, the panelists could not get beyond the fact that annuities are increasingly popular with consumers, and this may be a good time for many people to purchase an annuity.

“Consumers want the benefits of annuities there are more and more people are retiring now, something like 13,000 people turning 65 every day now without pensions and needing to self-fund retirements,” said Lau. “Annuities are really attractive to retirees providing guaranteed lifetime income.”

© Entire contents copyright 2024 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

MassMutual delivers record $2.5 billion dividend to policyholders

US catastrophe claims hit 7-year high, report finds

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Data on CDC and FDA Detailed by Researchers at University of New Hampshire (Long Covid Among Adults With Pre-existing Disabilities: Evidence From the 2022 National Health Interview Survey): CDC and FDA

- Digging deep: Who's funding Skagit's 2026 legislative, county races

- Atrium’s WakeMed acquisition faces new hurdle after State Health Plan decision

- New Arizona law provides clarity regarding firefighters’ health insurance

- Mid-year benefits review: What employers miss before renewal

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News